Banking

Getting to know the heart of the finance sector

Various forms of borrowing and lending have existed for millennia. But today’s commercial finance and investment banks can trace their roots to the merchant banks that grew at the end of the Middle Ages, while retail banks emerged in the seventeenth and eighteenth centuries with the development of fractional reserve banking and the standardised issue of what we now refer to as banknotes.

These were followed by other innovations – for which the City of London served as an important backdrop – including cheques, clearing houses, overdraft facilities and international finance.

By the early twentieth century, the importance and dangers of finance in the real economy were highlighted by a series of bank defaults and collapses in America, which eventually snowballed into the Great Depression. The response was tighter regulation, though within half a century this process was in reverse.

Following the global financial crisis of 2007-2008, in which financial institutions around the world collapsed or needed rescuing, banks were forced to boost their capital buffers and ring-fence their riskier operations from the more hum-drum work of retail banking. Hefty fines from governments for historic market manipulation, mis-sold products, reckless speculation and negligent oversight of operations all followed. Understandably, public trust in the sector sank.

More recently, the rise of mobile banking and technology has presented challenges to banks’ traditional focus on physical branches.

how do banks make money?

Banks make money from:

- Interest on lending

- Income from services, such as transactions

- Investment products (e.g M&A activity, helping companies or governments raise money, or trading securities)

- Insurance product

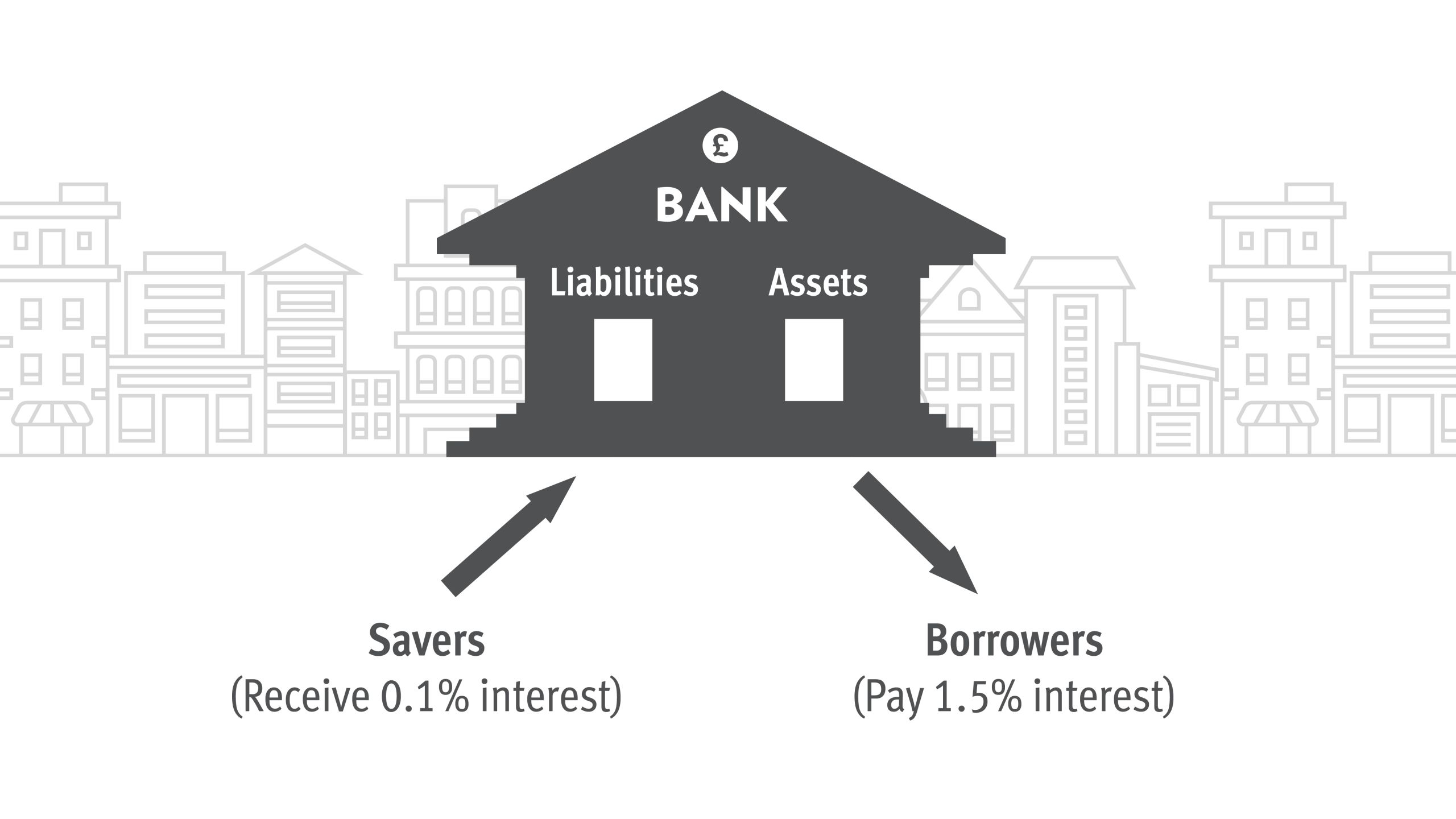

Banking, at its simplest, is about matching two groups of people: savers who want to keep their cash in a place that is safe and can earn some interest over the long-term, and borrowers who need cash to fund projects or purchases now.

To do this, a bank accepts deposits from the first group (the savers) and records these as liabilities on the balance sheet. These funds are then used to issue loans or advances to borrowers, which are recorded as assets.

For a bank to generate a profit, it needs to ensure the interest it receives from borrowers exceeds both the costs of running the bank and interest payments to depositors. It does this by charging a higher rate of interest to borrowers than it pays out to depositors. Anyone who has stored their money and taken out a mortgage with the same bank will know this all too well: your savings earn 0.1% interest, your borrowings cost 1.5%.

This sounds simple, but the reality is a complicated job of risk management because:

- Most deposits have been recycled into loans

- Only a fraction of deposits are actually reserved for withdrawal

This liquidity mismatch can lead to serious issues or bank runs if too many savers ask to pull their money at the same time.

Don’t forget economics

For a bank to make money, it must also navigate central banks’ interest rate-setting and constant shifts in economic fundamentals. These forces affect depositors’ rates of withdrawals or savings, and borrowers’ ability to pay back their loans in full, both of which impact a bank’s net interest margin – calculated as interest earned less interest paid out, divided by a bank’s average assets.

Business Models

The Bank of International Settlements (BIS) – sometimes referred to as the central bank of central banks – identifies three broad banking business models (which differ largely in the way that they are funded):

- Retail-funded commercial banks – which get most of their deposits from customers

- Wholesale-funded commercial banks – which rely more on interbank loans and debt for their deposits

- Capital markets-oriented banks – which are largely funded by wholesale markets, and whose assets comprise more tradeable securities than actual loans

the companies

Big banks

There are as many ‘market leaders’ in the world of banking as there are markets – which is to say a lot. If we define size by total assets, then China’s state-backed banking groups are now the largest lenders on the planet, according to S&P Global Market Intelligence’s most recent report. They are followed by the Japanese giant Mitsubishi UFJ Financial and HSBC (HSBA), whose London-listing belies an increasing pivot toward the Far East.

HSBC is also an interesting example of a lender with strong or leading positions in numerous geographical and product markets. In this sense, it both is and isn’t a peer of UK high-street names like Natwest (NWG) and Lloyds Banking (LLOY), which compete with HSBC and others as the largest providers of consumer and commercial loans in the UK.

Challenger Banks

Given their largely domestic focus, the largest UK-listed banks arguably face more competition from challenger banks such as Virgin Money (VMUK) and Metro Bank (MTRO) and smaller disruptive fintechs than they do large international firms.

US giants

Barclays remains an outlier in this regard, given its presence in investment banking on both sides of the Atlantic. That pits it against the trading desks and corporate finance teams of Wall Street, Goldman Sachs (NYSE:GS), Morgan Stanley (NYSE:MS) and Bank of America (NYSE:BAC) among them. Though perhaps pre-eminent in the world of US banking is JP Morgan (US:JPM), given its track record of superior returns and strong franchises in both corporate and consumer lending.

More competition please

In 2016, the UK’s Competition and Markets Authority concluded that retail banking was not competitive enough. The watchdog found that a large proportion of customers paid above-average prices for below-average services, and that banks weren’t motivated enough to improve. Instead of being broken up, the industry’s largest players were forced under the Open Banking directive to share their once secret datasets with market entrants.

Promoting fresh thinking and better use of technology and data are all welcome developments. But there’s little sign of this yet disrupting the dominance of the UK high street names over the mortgage or deposit-taking markets.

Further consolidation among the largest UK players therefore seems unlikely at this stage, even if cost-cutting is widely seen as the best way for executive teams to prop up battered profit margins. Going it alone is likely preferable to the headache of complicated competition probes, or the possibility of brand dilution a merger might bring. The situation is different in Europe, where the need to trim the fat in response to negative interest rate policies is acute.